Here are four questions (and answers) to help you make rational, well-informed rental investing decisions, and ensure your next rental property is a winner, including:

- How to best treat your rental expenses?

- Is your rental non-taxable?

- What are my state and federal tax withholding requirements?

- How does my LLC report in a non-communal property state?

How to best treat your rental expenses?

There are several considerations you need to examine in order to determine the best way to handle your rental expenses for tax purposes. It is not a matter of choice, however; the proper treatment is determined by the activities you perform. If you personally participated in the management of the property, then it is a matter of whether the property is subject to the vacation home rules.

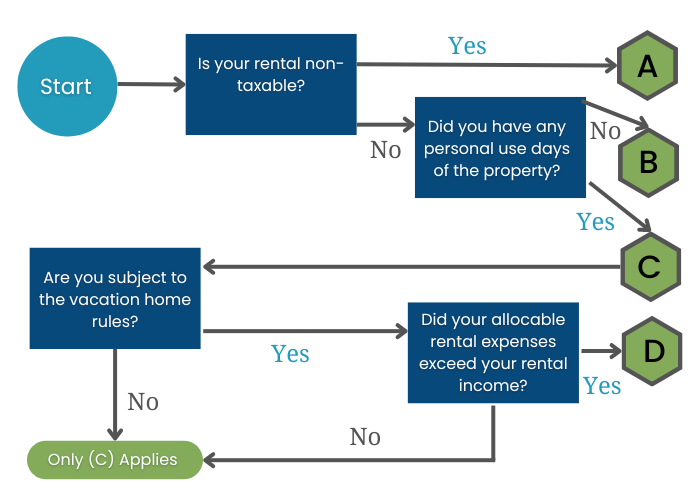

To help you find clarity on the proper treatment, refer to the decision chart below.

Is Your Rental Non-Taxable?

- Yes or No

- If Yes: See rules for Non-Taxable Rentals.

- If No: Do you have any personal use days on the property?

- If no, see the rules for Non-Personal Rentals.

- If yes, see the rules for Limited Use Percentage.

Are you subject to vacation home rules?

- If yes, and your allocable rental expenses exceeded your rental income, see the rules for Expense Limitations.

- If no, follow the rules for Limited Use Percentage.

Rules for Determining Selection

Non-Taxable Rentals

The casual rental of your personal home, that is renting for 14 days or less during the tax year, is non-taxable. As such, related expenses are not deductible. However, homeowners who have qualified mortgage interest and real property taxes can still be deducted on their Schedule A itemized deductions.

Non-Personal Use

If you and your family do not use the rental property during the year, qualified rental property expenses are fully deductible. Depending upon other factors, your deductions should be recorded either as a Schedule C business or on Schedule E of your Form 1040.

Expense Limitations Due to Rental Use

Just to complicate matters further, there are limitations on how you may deduct expenses on rental properties based on a formula that calculates your involvement, the number of rental days, and your personal use. Before completing Schedule E or Schedule C, review the formula to determine if limitations exist.

Your rental use percentage is based on the number of personal and rental use days as well as the square footage of the portion of the property that is rented.

To calculate the rental use percentage, consider:

Days Rented % = (Rental Use) ÷ [(Rental Use) + (Personal Use)] Area Rented % = (Sq. Footage Rented) ÷ (Overall Sq. Footage) Rental Use % = (Days %) x (Area %)

In addition, if the property is subject to the vacation home rules, and the amount of allocable expenses calculated using your rental use percentage exceeds the amount of rental income, please read the next rule which details expenses that exceed income.

Expenses Limited Due to Expenses Exceeding Income

If your expenses exceed your rental income and the vacation home rules, there are further limitations on what expenses will be permitted.

In a nutshell, if the above scenario exists, deductions for deprecation on the property cannot create a taxable loss. So, if your qualified mortgage interest and property taxes offset the rental income, you cannot claim operating expenses and deprecation against your income. However, you may be able to carry forward losses into future years when your income will hopefully be more substantial.

What are my state and federal tax withholding requirements?

If you rented your property through a third party, such as an app on the Internet, be certain to provide them with the appropriate tax ID/Social Security Number information in order for the third party to collect appropriate state and federal withholdings.

If you do not, you will need to pay this amount when you file, and it could lead to penalties if your overall income exceeds the IRS estimates. You will receive a 1099-K form from these third parties confirming the income you earned and any taxes withheld.

How does my LLC report in a non-communal property state?

If the property is held in LLC that you and your spouse are both members of and you do not live in a community property state, you will be required to file a Form 1065 partnership return to report your rental activities.

Parting Thoughts

From the casual renter to the owner of multiple rental units, most taxpayers are sadly disappointed that their rental ownership is not a Schedule C deduction windfall unless they can prove they have invested active hours of participation akin to operating any other business activity. The rules are complex, and the bar is set high for those seeking write-off opportunities.

Reach out to us if you have questions about your rental property and the tax considerations for it.