Often, we see inquiries from taxpayers who rent their home or vacation property for short-term or long-term occupancy, as well as investors who own one or more rental properties. They assume they will be able to treat their taxable losses as a business and file a Schedule C to reduce their adjusted gross income.

Unfortunately, this is probably not the case. To treat the unincorporated rental property as a business, the taxpayer must “materially participate” in the business. The IRS has several tests to determine if a business activity is active or passive.

Your Home is Probably Not a Business

If you rent your home to short-term rentals for more than 14 calendar days, you will be required to report this rental income on your 1040 tax return.

If you used a rental app or website as an agent for the rental, you may receive a Form 1099-K. Be aware that the amount you report on the 1099-K form is the gross amount and is exclusive of any refunds, adjustments, or service fees that may have been charged.

The good news is that these charges may be used as deductions on your tax return unless they are deemed to be non-taxable exceptions. Refunds, service fees, and adjustments are not included in the gross amount. These differences will be accounted for as deductions on your tax return.

The devil in all this is in the details. High-net-worth individuals looking to find big write-offs from renting their home will discover there are some complex conditions their rental activities must meet to be a deductible opportunity.

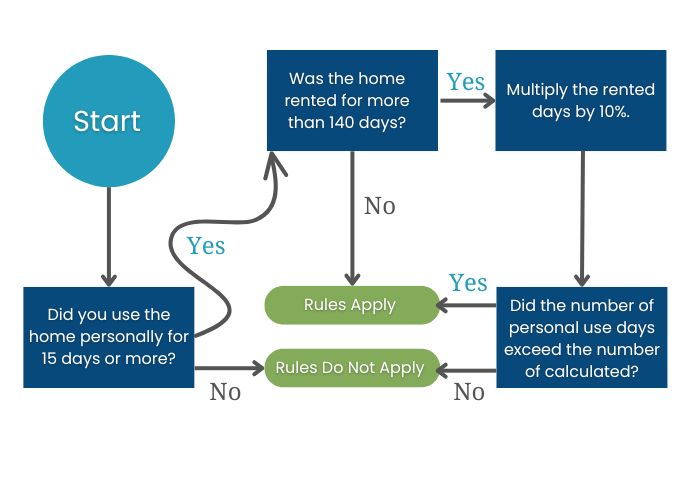

When it comes to short-term rentals, your behavior concerning rental activity can determine how gains and losses are treated by the IRS.

Your tax return files a rental property based upon activities. Short-term rentals typically fall into three classes, including

- Non-taxable rentals

- Schedule C rentals, or

- Schedule E rentals. (Most filers find that their rental activity should be reported on a Schedule E form.)

Let’s examine the differences between these three tax treatments:

Q: Did you personally stay at the property during the tax year?

- If no: Did you provide “substantial services” to your renters?

- If no, file a Schedule E

- If yes, file a Schedule C

- If yes, was the property rented for 14 or more days during the year?

- If yes, see the rules for filing under non-taxable.

- If yes, see the rules for filing under non-taxable.

Non-Taxable Rentals

Sometimes, people rent their homes for a few days during the year. In this scenario, your rental property may be treated as non-taxable, even if the rental dollar amount is significant. The rules are fairly straightforward. If the property was utilized as a residence by you during the year, and it was rented for less than 14 days, the rental is not taxable.

This is commonly referred to as the “Augusta Rule”, whereby people rent their home for only two weeks during a golf event. The IRS eventually agreed renting for 14 days or less does not require the income to be on a person’s 1040 tax return.

Taxpayers will be able to deduct property taxes and mortgage interest incurred on the property as they normally would on Schedule A.

Schedule C Rentals

Owners who provide what the IRS considers substantial services for guests in their rental qualify to report their income and deductions as a Schedule C business. However, as a Schedule C business, the taxable profits derived from this rental activity will also be subject to self-employment tax.

Schedule E Rentals

When the property owner does not provide what the IRS determines to be substantial services to their rental guests, rental income should be reported on Schedule E on their 1040. Taxable profits from a Schedule E are not subject to self-employment tax, and losses are limited to higher income earners based on the IRS limits for adjusted gross income.

If you have questions about claiming rental income, please give us a call.